Refractories Market Size, Share, Trends and Analysis Report – Global Opportunities & Forecast, 2025-2032

Refractories Market Overview

Refractories Market size reached USD 33.8 billion in 2024 and is estimated to reach USD 47.0 billion in 2032 and the market is estimated to grow at a CAGR of 4.2% from 2025-2032. The global refractories market growth is propelled by the rise in infrastructural development in developing countries, an increase in usage of glass, steel, and iron by the automotive industry, and growing consumption of non-ferrous materials.

Market Size, Forecast & Key Segment Insights

Market Size & Forecast:

-

- 2024 – USD 33.8 Billion

- 2032 – USD 47 Billion

- Market Forecast – CAGR of 4.2% from 2025-2032

Segment Insights:

-

- Form Type Insights: Shaped refractories captures the largest market share in 2024

- Alkalinity Type Insights: Acidic & Neutral Refractories hold the largest market share of the global refractory market

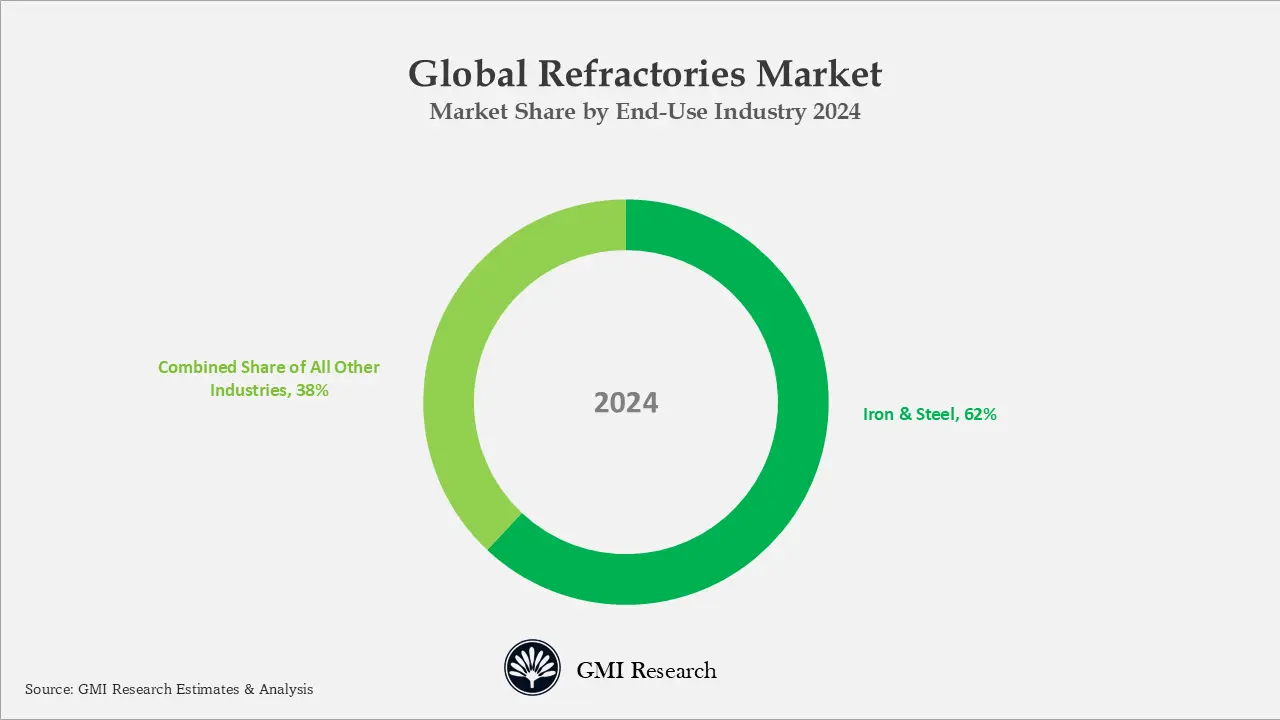

- End-Use Industry Insights : Iron & Steel Segment hold the Largest Market share of 62% in 2024

- Regional Market Insights: Asia Pacific Region Accounted for the Largest Market Share in 2024

Refractories Market Trends

Pus for Recycling Refractories

The push for using recycling refractory material is growing globally, the refractory materials that have been used and recycled to create secondary raw materials are referred to as refractory grogs. These can be classified into two types: low-quality and high-quality refractories. The usage of recycled refractories is conditional upon the quality of the original material, while 100% of high-quality recycled refractories can be employed in other procedures, only 0-30% of those obtained from low-quality refractories can be effectively used. The demand for recycling refractory goods has increased due to rising costs of raw materials and freight, coupled with environmental pressure encouraging businesses to look for more eco-friendly alternates for refractory applications are factors fostering the shift towards refractory recycling.

Refractory Market Growth Drivers

Rise in Urbanization Driving Infrastructure & Construction Boom

The rise in urbanization and industrialization, particularly in emerging economies like China and India, has prompted substantial investments in commercial and residential construction. Global Construction Perspective and Oxford Economies project an 85% growth of USD 15.55 trillion by 2030. China, the US, and India are estimated to contribute, accounting for 57% of overall global growth.

In addition, China is one of the fastest-growing countries is propelling an increased demand for travel, requiring continuous development of roadways, and railways. This, in turn, has contributed to rising growth of the automotive industry across China.

The rise in infrastructure development in developing countries or commercial and residential buildings, is thereby projected to foster the demand for refractories in the iron and steel and cement industries. The growing construction activities in these countries are also projected to drive the steel, glass industry, thereby driving the refractories demand and requiring more refractory lining replacements and new installations.

Growth of the Iron & Steel Industry

The steel industry is the largest consumer of refractories, accounting for 62% % of market share globally. When it comes to overall steel production cost refractories represent only 2–3%, however refractories are indispensable, as no steel can be produced without them.

In steel industry refractories are used in line furnaces, ladles, and tundishes, they endure intense heat and corrosive slag, requiring frequent replacement. As steel production is very demanding, selecting between brick and monolithic refractories depends on operational needs, installation requirements, and performance expectations for each type.

Recovery in The Automotive Sector

The automotive industry’s recovery, propelled by a rise in electric vehicles, has generated momentum for vehicle manufacturing materials including iron, glass, and steel. As per the report by World Steel Association, and the International Organization of Motor Vehicles suggested that steel-based products comprise 60% of a vehicle’s body structure. Whereas, Glass, constituting >6% of the vehicle’s body weight, is an important component. The growing demand for materials such as glass and steel from the automotive industry has fostered by their significance in manufacturing. Consequently, the growth of the automotive industry is projected to contribute to the growth of the refractories market globally.

Although to address the future fuel economy demands, automotive industry the is discovering innovative solutions, prompting continuous investments in advanced materials by the steel industry. This has resulted in the introduction of an innovative variation of innovative steel tailored for the automotive sector.

The development of Advanced High Strength Steel has proven important in helping the automotive industry address growing regulatory standards. Moreover, yearly introductions of new car models incorporating higher-strength steel components, lightweight, offer a cost-effective solution to the rising need for enhanced safety and fuel economy. The automotive industry’s increasing adoption of improved steel is fostering product demand.

Growing Demand From Power & Petrochemical Industries

Refractories are witnessing demand in the power generation sector, specifically for applications in the inside lining, boilers, and other critical locations. The growth in power generation can be attributed to the global demand for power, renewable energy expansion, and a growing usage of sustainable solutions for the future.

As per the Energy Information Administration, geothermal electricity generated touched 15.89 billion kilowatt hours during 2020, somewhat lower than the 16.22 billion kilowatt hours during 2019. In addition, the Central Electricity Authority predicts India’s power demand to reach 817 GW by 2030.

The thriving power generation sector is propelling demand for refractory materials such as aluminum oxides, zirconium silicate, sillimanite, and many more across different applications in the power industry, resulting in growth opportunities in the global market.

Refractories plays an essential role in oil and gas operations for protecting equipment from extreme heat and chemicals, refractories demand from petroleum industry is increasing due to petrochemical growth, stricter regulations, and the drive for higher energy efficiency.

Challenges Faced by Refractories Market Companies

Meanwhile, the manufacturing process of refractories involves the emission of organic particulate matter and different harmful gases, including nitrogen oxides, fluorides, carbon dioxide, volatile organic compounds, and sulfur dioxide.

Particulate Matter emissions result from procedures such as grinding, drying, calcining, and crushing, while gases and VOCs are released during firing and tar & pitch operations, respectively. In the United States, regulations govern the disposal of refractory waste and provide guidelines for refractory use, encouraging the recycling of chrome-based refractories, particularly prevalent in the iron & steel industry.

In Europe, initiatives such as ReStaR focus on developing the reliability and precision of present refractory testing standards. Environmental regulations and restrictions on refractory material use serve as limitations on the growth of the refractory market.

Global Refractories Market Segment Analysis

Form Type Market Insights: Shaped refractories captures the largest market share in 2024

Shaped refractories lead the global refractories market because of its precise dimensions, consistent quality, and dependable performance in high-temperature environments. Their standardized design ensures easier installation, reduced downtime, and strong structural integrity under thermal and mechanical stress. Shaped refractories are extensively used in steel, cement, and glass industries, their long service life, broad availability, and versatility further strengthen their dominant position.

Refractory bricks market growth is driven by owing to its widely used in steel, cement, glass, and kiln applications, with demand rising due to industrial growth in emerging economies. High-alumina bricks dominate because of their superior heat and corrosion resistance, followed by fireclay, magnesia, and silica types. Competition remains strong as manufacturers innovate for better efficiency, durability, and sustainability.

Alkalinity Type Market Insights: Acidic & Neutral Refractories hold the largest market share of the global refractories market

Acidic refractories like (like silica and fireclay bricks) and neutral refractories are very popular and hold the largest market share owing to its greater use than basic refractories due to their wider chemical compatibility, lower production costs, and suitability across a broader range of industrial applications. Acidic and neutral refractories dominate a wide range of industries, including glass manufacturing, cement production, non-ferrous metallurgy, petrochemical furnaces, incinerators, and general industrial heating systems.

End-Use Industry Market Insights : Iron & Steel Segment hold the Largest Market share of 62% in 2024

The iron & steel segment dominate the market share and it projected to drive the market revenues forecast period due to its extensive applications in reactors, furnaces, and vessels in steel manufacturing. In addition, the frequent replacement in the iron and steel industry of refractory lining, occurring every 30 minutes to two days in dissimilar stages of the manufacturing procedure, leads to substantial consumption.

The advancement in glass melting technology relies largely on the high performance and progress of refractory products. Selecting refractories is important in the construction of a glass furnace, as the furnace’s longevity is directly tied to the quality of refractories. Alumina Zirconia Silica serves as the primary structural refractory material for glass furnaces, due to its resistance to wetting by molten glass and minimal reactivity with it. The rising glass industry, influenced by the shift to sustainable alternatives from plastics, is driving an increased demand for refractories.

Dependable refractory solutions are essential for improving efficiency in cement manufacturing. Rotary kilns within the cement industry employ refractory bricks, while monolithic refractory is applied in higher wear areas, typically at the outlet of cement kilns. In the pre-heater section of cement plants, dense castables line cyclones owing to their wear resistance and compatibility with complex shapes. Beyond cement, refractory applications extend to petrochemicals, boilers, military, light, machinery, electric power, and other industries.

Regional Market Insights: Asia Pacific Region Accounted for the Largest Market Share in 2024

The Asia Pacific region is projected to dominate the largest share of the global market due to the robust growth across various end-use industries. Asia Pacific contributes >70% to global steel production, and China alone contributes approx. 50% as per the World Steel Association. In addition, the region’s presence in cement and non-ferrous metal industries further solidifies its leading position in the global market.

In addition, the robust demand for refractories in the Asia Pacific region is propelled by thriving sectors such as metallurgy, power generation, and cement. The growing usage of refractories in different facets of cement production, including kiln hoods, grate coolers, preheaters, riser ducts, and others, significantly contributes to market growth. Cement output in China is anticipated to steady at 1-1.5 billion tons by 2030, driven by increased production for construction and infrastructure projects. The growth of refractories in the Asia Pacific region is primarily propelled by different applications, especially construction leading the APAC refractories market growth opportunities in the forecast period.

Refractories Market Major Players & Competitive Landscape

Several leading companies are RHI Magnesita GmbH, Vesuvius, Krosaki Harima Corporation, Shinagawa Refractories Co., Ltd., Saint-Gobain, Coming Incorporated, Morgan Advanced Materials plc, CoorsTek Inc., Harbisonwalker International, and Imerys Refractory Minerals, among others.

Key Refractories Market Developments

-

- In 2023, INTOCAST AG successfully acquired EXUS Refractories S.p.A, to update an innovative technological advancement in its production unit which further reinforced its position in the market.

- In 2023, RHI Magnesita GmbH announced an acquisition of Dalmia Bharat Refractories Limited’s Indian refractory business to address the growing demand from end-use industries.

- In 2021, ArcelorMittal Refractories, collaborated with Krosaki Harima Corporation. The collaboration is intended to optimize production capacities and expand ArcelorMittal Refractories’ product portfolio using Krosaki Harima’s manufacturing technology.

- In 2021, Imerys initiated production at its new Vizhag refractory plant with an investment of INR 350 crores to cater the demand of local customers. The new plant will supply the refractory and the construction market with calcium aluminate binders.

- In 2021, the Refratechnik Group collaborated with Höganäs Borgestad Group for the supply of refractory products.

- In 2020, Carbo Sun Luis was acquired by Morgan Advanced Materials plc successfully in order to support and expand the network in Argentina, and Chile.

- In 2020, Morgan Advanced Materials plc successfully acquired of Carbo Sun Luis to support and grow the network in Chile, Argentina, and Chile.

- In 2020, Vesuvius introduced its new product – KALPUR. It is a Direct pouring application on an Automatic High-Pressure Green Sand Moulding Line and have improved yield and directional solidification.

- In 2019, RHI Magnesita invested EUR 40 million for the building of new Dolomite Resource Centre Europe. This center will be used in the entire European market for mining and processing at the Hochfilzen site in Tyrol before being transported by rail to France.

Refractories Market Scope of the Report

|

Report Coverage |

Details |

| Market Size Value in 2024 |

USD 33.8 Billion |

| Market Revenue Forecast in 2032 |

USD 47.0 billion |

| CAGR |

4.2% |

| Market Base Year |

2024 |

| Market Forecast Period |

2025-2032 |

| Base Year & Forecast Units |

Revenues (USD Billion) |

| Market Segment | By Form, By Alkalinity, By End-Use Industry, By Region |

| Regional Coverage | Asia Pacific, Europe, North America, and RoW |

| Companies Profiled | RHI Magnesita GmbH, Vesuvius, Krosaki Harima Corporation, SHINAGAWA REFRACTORIES CO., LTD., Saint-Gobain, Coming Incorporated, Morgan Advanced Materials plc, CoorsTek Inc., Harbisonwalker International, and Imerys Refractory Minerals, among others; a total of 10 companies covered. |

| 25% Free Customization Available | We will customize this report up to 25% as a free customization to address our client’s specific requirements |

Refractory Industry Market Analysis Report Segmentation

The global refractories market has been segmented based on form, alkalinity, end-use Industry, and regions. Based on Form, the market is segmented into shaped refractories & unshaped refractories. Based on alkalinity, the market is segmented into acidic & neutral refractories and basic refractories. Based on end-use Industry, the market is segmented into iron & steel, power generation, non-ferrous metal, cement, glass, other industries.

Global Refractories Market by Form

-

- Shaped Refractories

- Unshaped Refractories

Global Refractories Market by Alkalinity

-

- Acidic & Neutral Refractories

- Basic Refractories

Global Refractories Market by End-Use Industry

-

- Iron & Steel

- Power Generation

- Non-Ferrous Metal

- Cement

- Glass

- Other Industries

Global Refractories Market by Region

-

-

North America Refractories Market

- By Form

- By Alkalinity

- By End-Use Industry

- US Market All-Up

- Canada Market All-Up

-

Europe Refractories Market

- By Form

- By Alkalinity

- By End-Use Industry

- UK Market All-Up

- Germany Market All-Up

- France Market All-Up

- Spain Market All-Up

- Rest of Europe Market All-Up

-

Asia-Pacific Refractories Market

- By Form

- By Alkalinity

- By End-Use Industry

- China Market All-Up

- India Market All-Up

- Japan Market All-Up

- Rest of APAC Market All-Up

-

RoW Refractories Market

- By Form

- By Alkalinity

- By End-Use Industry

- Brazil Market All-Up

- South Africa Market All-Up

- Saudi Arabia Market All-Up

- UAE Market All-Up

- Rest of world (remaining countries of the LAMEA region) Market All-Up

-

Major Players Operating in the Refractories Market

-

-

RHI Magnesita GmbH

-

Vesuvius

-

Krosaki Harima Corporation

-

SHINAGAWA REFRACTORIES CO., LTD

-

Saint-Gobain

-

Coming Incorporated

-

Morgan Advanced Materials plc

-

CoorsTek Inc

-

Harbisonwalker International

-

Imerys Refractory Minerals

-

Frequently Asked Question About This Report

Refractories Market [UP1989-001001]

Refractories Market size was estimated at USD 33.8 billion in 2024.

Global Refractories Market growth is driven by rise in urbanization driving infrastructure & construction boom, growing demand for iron & steel, recovery in the automotive sector, growing demand from power & petrochemical industries.

Refractories Market provides ample opportunities and it is estimated to reach USD 47.0 billion in 2032 and the market is estimated to grow at a CAGR of 4.2% from 2025-2032.

Major players operating in the market are RHI Magnesita GmbH, Vesuvius, Krosaki Harima Corporation, Shinagawa Refractories Co., Ltd., Saint-Gobain, Coming Incorporated, Morgan Advanced Materials plc, CoorsTek Inc., Harbisonwalker International, and Imerys Refractory Minerals, among others.

Asia Pacific region is projected to dominate the largest share of the global market due to the robust growth across various end-use industries

Iron & steel segment dominate the market with a market share of 62% in 2024 and it projected to drive the market revenues forecast period

Shaped refractories captures the largest market share in 2024.

Related Reports

Why GMI Research