Armored Vehicles Market Size, Share, Trends and Growth Report – Global Opportunities & Forecast, 2026–2033

Armored Vehicles Market Overview

Armored Vehicles Market size was reached USD 40.5 billion in 2025, and the market is forecast to touch USD 53.7 billion in 2033, growing at a CAGR of 3.6% from 2026-2033 primarily driven by rising defense budgets & military modernization globally, rise in the number of geopolitical conflicts & instability worldwide, technological advancements (ai, autonomous & hybrid systems).

Market Size & Forecast:

-

- 2025 – USD XX Billion

- 2033 – USD XX Billion

- Market Forecast – CAGR of XX% from 2026-2033

Key Segment Insights:

-

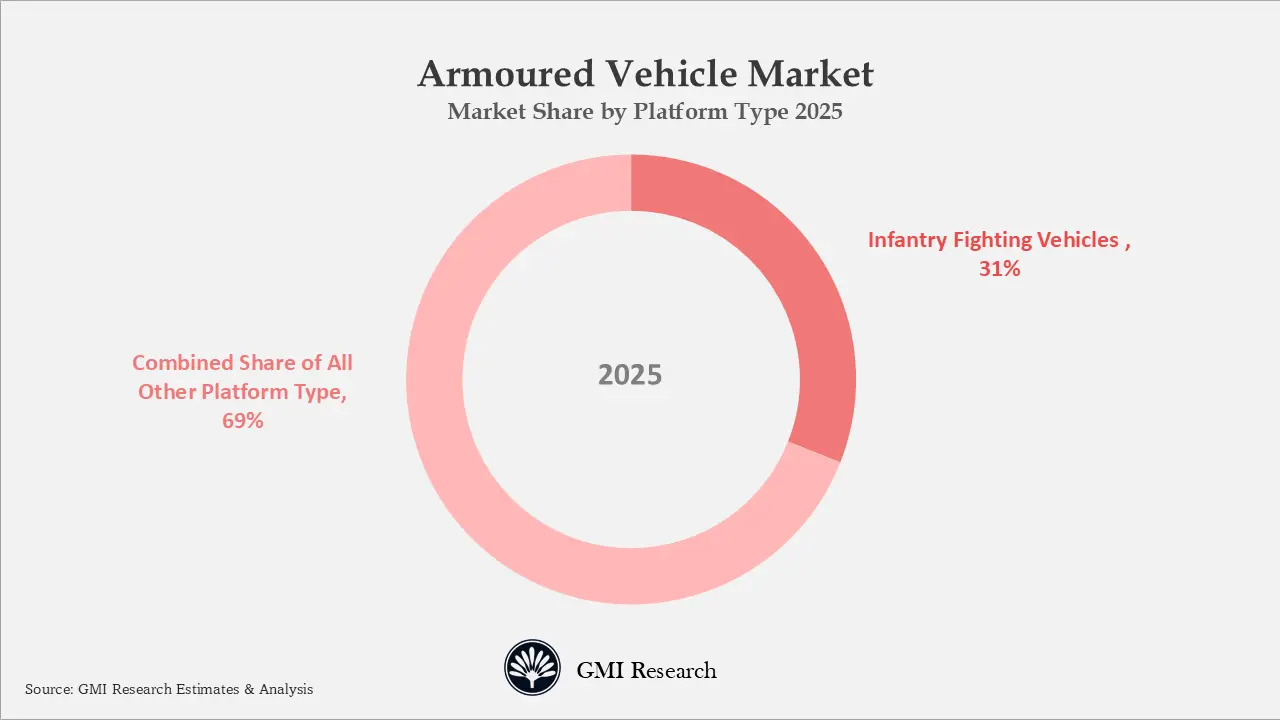

- Platform Type Insights: Infantry Fighting Vehicles (IFVs) accounted for the largest share, holding 31% of the market in 2025.

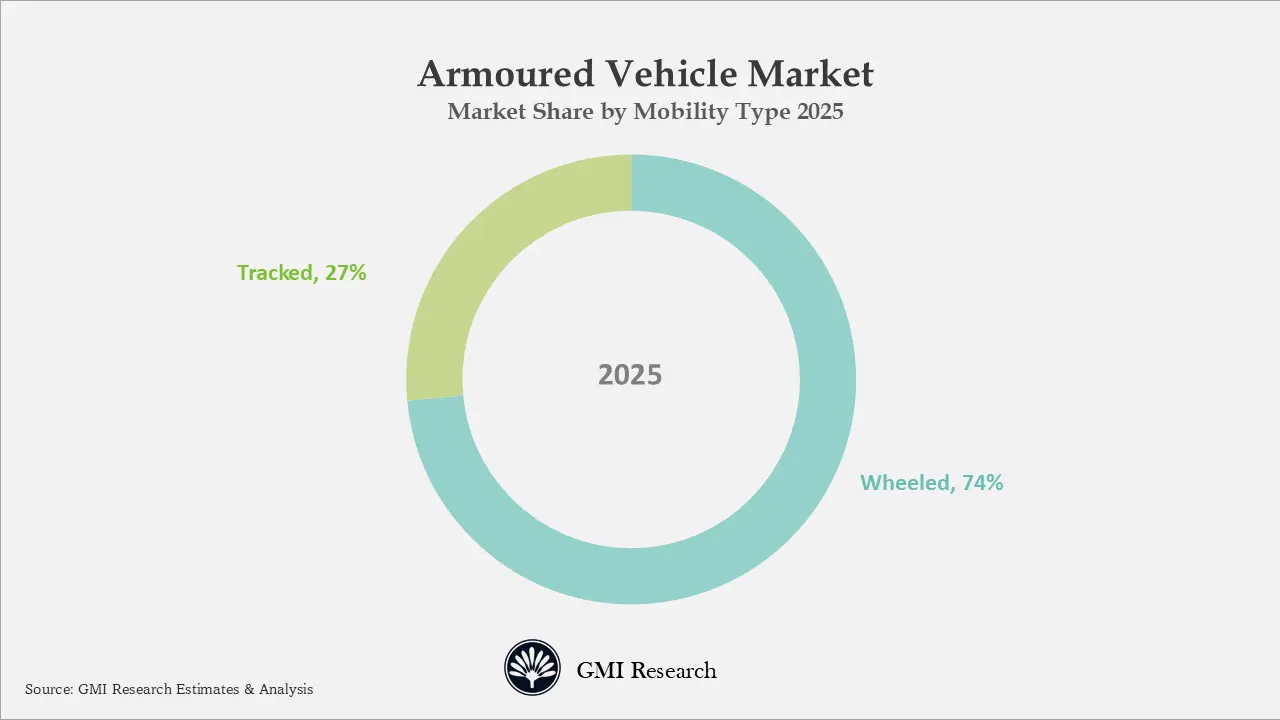

- Mobility Type Insights: Wheeled armored vehicles dominated the global revenues with a 73.5% share in 2025.

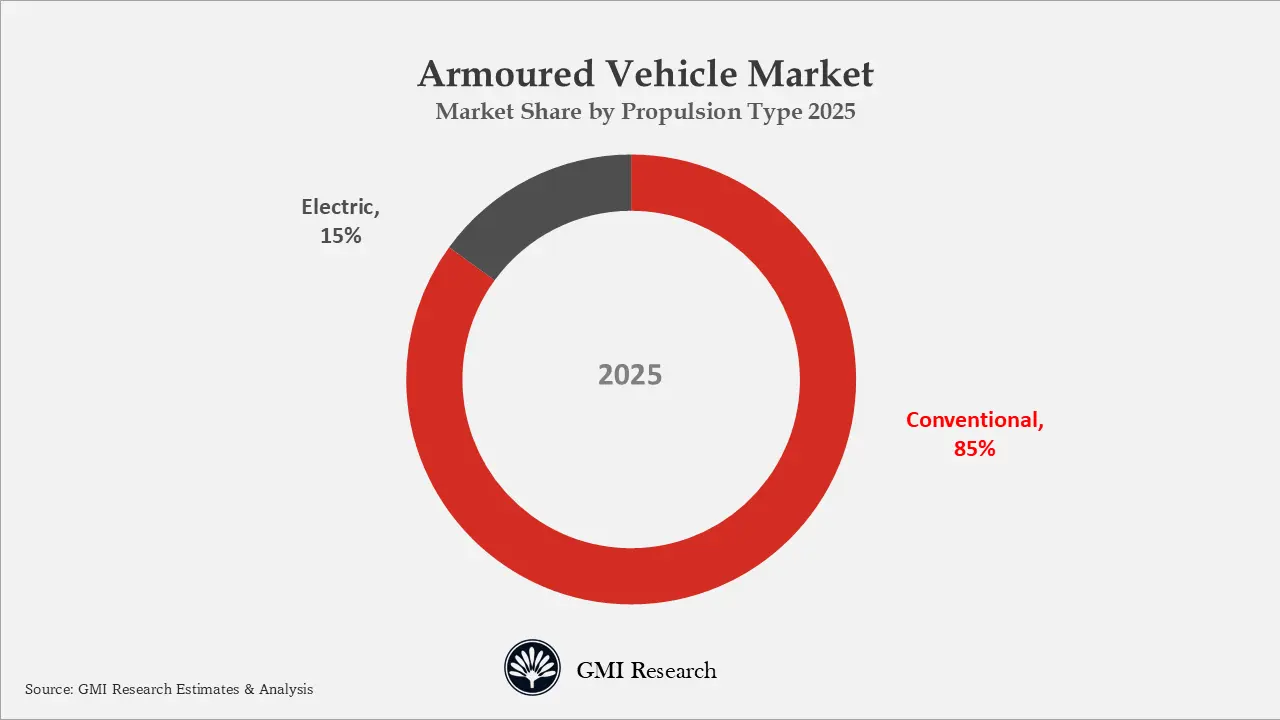

- Propulsion Type Insights: Conventional propulsion vehicles led the market, contributing more than 85% of total revenue in 2025.

- Point of Sales Insights: The OEM segment held the largest market share in 2025.

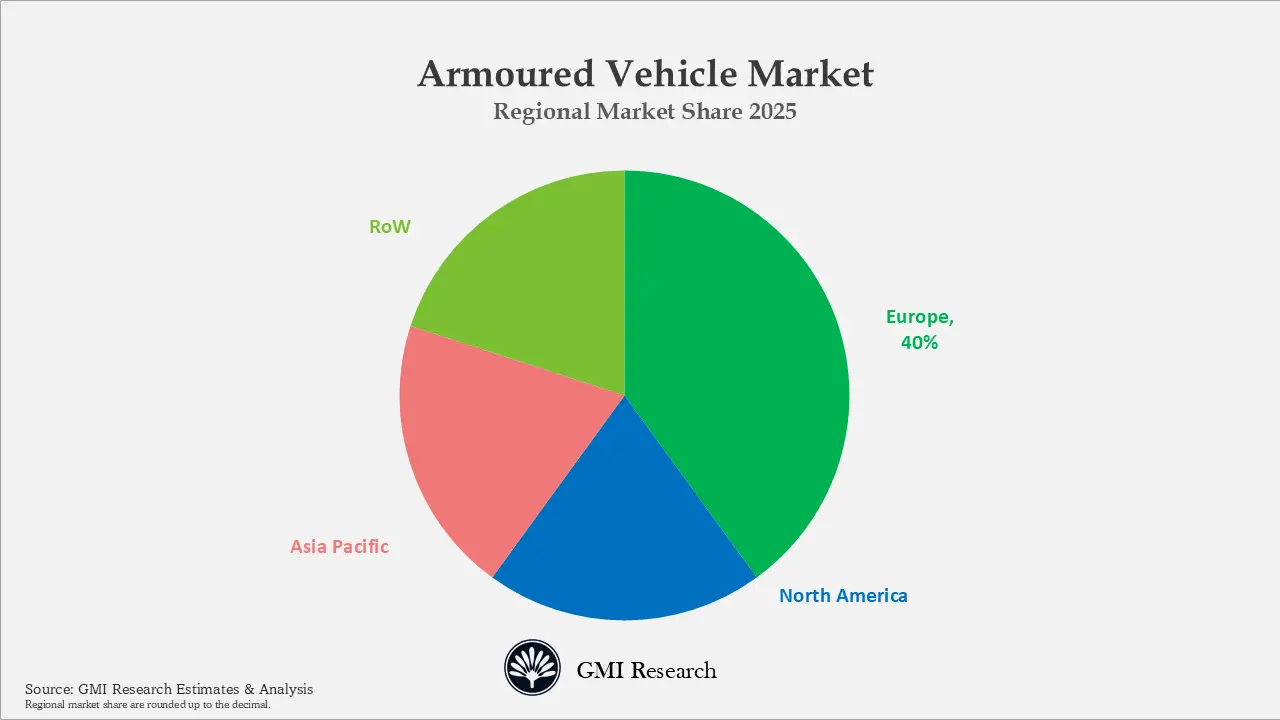

- Regional Analysis: Europe dominates the global market revenues in 2025

Armored Vehicles Market Trends

The growing adoption of unmanned systems in military operations by defense forces around the globe is predicted to result in market opportunities for the expansion of the global armored vehicle market. Innovations in the transmission medium, navigation, surveillance, protection, adaptability, and increased situational awareness are predicted to further improve growth opportunities for armored vehicles. The growing demand for unmanned systems is extensively used by military forces in different nations for combat functions and intelligence. Surveillance and Reconnaissance is projected to propel the global armored vehicles market growth.

The demand for fuel-efficient armored vehicles, driven by fluctuating fuel prices, presents different growth opportunities for companies in the global armored vehicle market. Producers are making efforts towards developing hybrid or electric armored vehicles to decrease fuel consumption and develop overall performance. The increasing shift towards clean energy is expected to foster the demand for electric or hybrid-engine armored vehicles among both defense and commercial end-users in the forecast period. In addition, rising government engagement and investment in improved electric vehicles will facilitate the development of fuel-efficient armored vehicles, delivering growth opportunities for industry players.

Armored Vehicles Market Growth Drivers

Rising Defense Budgets & Military Modernization Globally

In recent years the global military expenditure has surged to unprecedented levels, driven by sharp increases in spending across Europe and the Middle East region and the recent US, Israel and Iran conflict is pushing the increase in the defence budget envelope further in the coming years. As per Sipri, the global defence spending reached USD 2.7 trillion in 2024 increased by 9.4% over 2023, spending on military spending increased across all regions

As per the Sipri report the global defence spending is highly concentrated and the top five countries accounted for over 60% of total global defence expenditure equivalent to USD 1.6 trillion in 2025. The United States leads with nearly USD 1 trillion in 2025, followed by China at USD 330 billion and Russia at USD 160 billion, Germany USD 90 billion and India USD 86 billion. Other significant spenders include the UK, Saudi Arabia, France, Japan, and South Korea, collectively shaping global security dynamics, defence contracts, and advanced technology supply chains. The largest increase witnessed in Europe as the miltary spending in Europe, including Russia, surged 17% to USD 693 billion in 2024, driving global growth, The surge in defense spending by Nato countries is primarily driven by Russian and Ukraine conflict and also by strong pressure from the U.S., NATO allies agreed in June 2025 to raise defence spending to 5% of GDP by 2035, more than doubling the previous 2% target. Amid a growing sense of global insecurity leading torising defence budgets will drive demand for armored vehicles in the coming years.

Rise in the number of Geopolitical Conflicts & Instability Worldwide

In the last couple of years the world has entered into the era of intense competition for resource and to maintain hegemony. This is marked by escalating, interconnected, and rapidly evolving global risks.

A contested multipolar world has taken shape pushed by Russia and China with some supports from the global south countries, where rising confrontation hinders collaboration, and trust and the foundation of cooperation is steadily eroding. The war in Ukraine work as catalyst for global insecurity followed by Israel genocide in Gaza and eventually the attack by US & Isarel has amplified the geopolitical insecurity.

Air power is a critical element of modern warfare, yet it is inherently constrained by its inability to control or hold territory, achieve decisive sustained victories on its own. In order to hold and maintain control over a territory a ground based force is required and armored vehicle plays a big role in attacking, conquering and holding territory make its an integral parts of modern warfare.

The global armored vehicle market is observing growth, driven by the increase in asymmetric warfare. In addition, the militarization of law enforcement agencies and a rise in cross-border disputes are key drivers of increased demand for armored vehicles in the forecast period. Furthermore, the necessity to reduce the size and develop the effectiveness of vehicles in the defense sector, coupled with the growing demand for robust, highly efficient, and combat US armored vehicles, will continue the growth of the global market. The escalation of asymmetric warfare globally is attributed to factors such as economic conditions, political instability, and religious, and socio-cultural concerns. The rise in asymmetric warfare has turned into an increase in government agencies’ demand to implement Bradley armored vehicles as they offer advanced prevention against ballistic attacks and blasts.

Technological Advancements (AI, Autonomous & Hybrid Systems)

Advancements in armored vehicles are increasingly driven by software-defined architectures that enable real-time data processing, improved situational awareness, and faster decision-making. Integration of virtualization, open systems, and DevSecOps practices enhances system flexibility, security, and scalability. Continuous software updates, simulation capabilities, and edge computing allow rapid deployment of new features, reduce lifecycle costs, and support interoperability, transforming vehicles into more adaptive, connected, and mission-ready platforms.

Armored Vehicles Market Segment Analysis

Platform Type Market Insights: Infantry Fighting Vehicles (IFVs) platforms type captured the largest market share of 31% in 2025.

Infantry Fighting Vehicles (IFVs) platforms type hold the largest market share of 31% in 2025 as infantry fighting vehicle functions as the primary combat platform for armored, mechanized, and motorized infantry, as well as broader land force units. IFVs play a crucial role in modern warfare, combining firepower, mobility, and protection in a single platform. The demand for IFVs is projected to rise during the coming years, with emphasis on platforms that balance cost-efficiency with advanced technological capabilities.

Main Battle Tanks (MBTs) are still find relevance in today’s warfare owing to combination of features such as their armour, mobility, and firepower ensures they remain indispensable assets. The global political uncertainty and significant increase in Europe defence expenditure and other parts of the world will drive the demand for MBTS during the forecast period.

Mobility Type Market Insights: Wheeled armored vehicles types dominates the global market revenues with a market share of 73.5% in 2025

Wheeled armored vehicles types holds a market share of 73,5% owing to as it offer enhanced on-road mobility, lower maintenance demands, and reduced fatigue for crews. Additionally, they are easier to repair and generate less noise during movement, largely due to reduced vibration and minimal metal-to-metal contact in their running gear.

Tracked armored captures a market share of 26.5% in 2025 and is more preferred from mobility standpoint, tracked vehicles provide the most effective solution for versatile platforms operating across varied and challenging terrains. They excel in off-road performance, accommodate weight growth, and enhance battlefield survivability and combat effectiveness.

Propulsion Type Market Insights: Conventional propulsion armored vehicles accounted for the largest revenues with a market share of 85% in 2025

Conventional propulsion armored vehicles holds the largest market share of 85% in 2025 as these vehicles are continue to be favored by military forces for their high energy density, dependable performance in harsh conditions, and well-established logistical support networks.

However electric propulsion armored vehicles captures around 15% of the market share in 2025 and is projected to grow at a higher CAGR during the forecast period as llectric armored vehicles show future potential as battery and charging technologies improve. However, current limitations in range, durability, and logistics restrict their suitability, making widespread military deployment challenging at present.

Point of Sales Type Market Insights: OEM segment captures the largest market share in 2025.

OEM segment held the largest market share in 2025 owing to as most of the military equipment are by defence department directly from the OEM in a long term service contracts. As the way the has been fought has been changing in the recent years the development of new armored vehicles to counter the present challenges faced by armoured vehicle will drive this segment growth during the forecast period.

Regional Analysis: Europe dominates the global market revenues in 2025

Europe has emerged as the largest market for armoured vehicle globally owing to Russia and Ukraine war. Push from the US government to European Nato countries to increase their defence budget initially to 2% but eventually to 5% of the GDP by 2035 is driving demand for military equipment in the region. Large number of armoured vehicles ordered has been placed by regional countries.

Asia-Pacific region is projected to witness a robust growth due to an increase in military investments among countries across APAC. The rise in geopolitical tensions, countries including India, Singapore, South Korea, China, and Japan are making investments in acquiring new armoured vehicles to change the aging fleets that have been in action for over 30 years.

Middle East region is also projected to grow at a high growth rate during the forecast period due to the current US, Isarel and Iran conflict. The demand for armoured vehicle is forecast to increase as Saudi Arabia and UAE have massive defence budgets due to rising regional instability which has driven the need for enhanced security measures to protect VIPs, diplomats, and critical infrastructure.

Armored Vehicles Market Major Players & Competitive Landscape

Several leading companies are Rheinmetall AG, BAE Systems, General Dynamics, Oshkosh Corporation, Hanwha Group, KNDS, Otokar Otomotive Ve Savunma Sanayi, Textron Inc., Krauss-Maffei Wegmann, Denel SOC Ltd., Textron Systems Corporation, Elbit Systems, Patria Group, FNSS Savunma Sistemleri AS, Arquus, Hyundai Rotem among others.

Key Armored Vehicles Market Developments

-

- In 2025, Germany is gearing up for a new wave of multi-billion-euro defense procurements, including 20 Eurofighter jets, up to 3,000 Boxer armoured vehicles, and approximately 3,500 Patria infantry fighting vehicles. The Eurofighter deal alone is projected to be valued between Euro 4 billion and Euro 5 billion, according to sources. Meanwhile, the Boxer vehicles manufactured by KNDS and Rheinmetall are estimated at around Euro 10 billion, while the Patria vehicles are expected to cost roughly Euro 7 billion.

- In 2025, The government of Netherlands has agreed to procure at least 46 Leopard 2A8 tanks from KNDS, marking the country’s return to operating a dedicated tank unit after more than a decade. The Dutch government confirmed that deliveries are scheduled between 2028 and 2031. This acquisition is part of a broader effort to strengthen defense capabilities and align with NATO commitments, including the target of allocating at least 2% of GDP to military spending.

- In 2023, The U.S. Army Contracting Command Detroit Arsenal announced a content with A.M. General to produce nearly 10,000 trailers coupled with 20,000 Joint Tactical vehicles for the armed forces of the U.S.

- In 2023, The Italian Navy awarded a signed agreement to IVECO Defense Vehicles to offer Amphibious Armored Vehicles Personnel Carriers which further strengthen the force and navy of the San Marco Marina Brigade.

- In April 2022, Rheinmetall AG, a German arms manufacturing company announced that it has received contract from UK Ministry of Defense for manufacturing 4 Rheinmetall Mission Master SP surveillance Autonomous Unmanned Ground Vehicles (A-UGV) and 3 Rheinmetall Mission Master SP cargo vehicles, which makes up total of 7 new A-UGVs.

- In April 2022, Lithuania’s Defence Ministry announced declared its plans to procure more than 120 boxer infantry fighting vehicles to expand the country’s modern fleet of infantry fighting vehicles.

- In June 2021, Katmerciler announced that it has received contract to provide 118 Hızır 4×4 tactical wheeled armored vehicles to Kenya. This contract helped Katmerciler to expand its footprint in the African market.

- In February 2021, Bharat Forge, an engineering and technology company, entered into a strategic partnership with international aerospace and technology conglomerate Paramount Group to manufacture armoured vehicles in India.

- In March 2020, BAE System was awarded contract worth USD 339 million for manufacturing 48 vehicle sets of M109A7 Self-propelled Howitzer (SPH) and M992A3 Carrier, Ammunition, Tracked (CAT) vehicle, to increase the overall combat capability of Armored Brigade Combat Teams (ABCTs).

Key Armored Vehicles Market outlook

The outlook for global market for armored vehicles looks promising and as per the GMI Research the armored vehicles market size 2025 reached USD 40.5 billion and the market is projected to touch USD 53.7 billion in 2033. The market is projected to grow owing to steady, defense-driven growth over the forecast period, supported by modernization programs, geopolitical tensions, and technological evolution.

Armored Vehicles Market Scope of the Report

|

Report Coverage |

Details |

| Market Size Value in 2025 |

USD 40.5 billion |

| Market Revenue Forecast in 2033 |

USD 53.7 billion |

| CAGR |

3.6% |

| Market Base Year |

2025 |

| Market Forecast Period |

2026-2033 |

| Base Year & Forecast Units |

Value (USD Billion) |

| Market Segment | By Platform Type, By Mobility, By Propulsion, By Point of Sale, By Region |

| Regional Coverage | Asia Pacific, Europe, North America, and RoW |

| Companies Profiled | Rheinmetall AG, BAE Systems, General Dynamics, Oshkosh Corporation, Hanwha Group, KNDS, Otokar Otomotive Ve Savunma Sanayi, Textron Inc., Krauss-Maffei Wegmann, Denel SOC Ltd., Textron Systems Corporation, Elbit Systems, Patria Group, FNSS Savunma Sistemleri AS, Arquus, Hyundai Rotem, among others, a total of 16 companies covered. |

| 25% Free Customization Available | We will customize this report up to 25% as a free customization to address our client’s specific requirements |

Armoured Vehicle Industry Analysis Report Segmentation

The Global Armored Vehicles Market has been segmented on the basis of Platform Type, Mobility, Propulsion, Point of Sale and Region. Based on the Platform Type, the market is segmented into Armored Personnel Carriers (APCs), Infantry Fighting Vehicles (IFVs), Mine-Resistant Ambush-Protected (MRAP), Main Battle Tanks (MBTs), Tactical and Support Vehicles, Autonomous Ground Vehicles (AGVs), and Others. Based on the Mobility, the market is segmented into Wheeled and Tracked. Based on the Propulsion, the market is segmented into Conventional and Electric. Based on the Point of Sale, the market is segmented into OEM and Retrofit.

Global Armored Vehicles Market by Platform Type

-

- Armored Personnel Carriers (APCs)

- Infantry Fighting Vehicles (IFVs)

- Mine-Resistant Ambush-Protected (MRAP)

- Main Battle Tanks (MBTs)

- Tactical and Support Vehicles

- Autonomous ground vehicles (AGVs)

- Others

Global Armored Vehicles Market by Mobility

-

- Wheeled

- Tracked

Global Armored Vehicles Market by Propulsion

-

- Conventional

- Electric

Global Armored Vehicles Market by Point of Sale:

-

- OEM

- Retrofit

Global Armored Vehicles Market by Region

-

-

North America Armored Vehicles Market

- US Market

- Canada Market

-

Europe Armored Vehicles Market

- UK Market

- Germany Market

- France Market

- Spain Market

- Rest of Europe Market

-

Asia-Pacific Armored Vehicles Market

- China Market

- India Market

- Japan Market

- Rest of APAC Market

-

RoW Armored Vehicles Market

- Brazil Market

- South Africa Market

- Saudi Arabia Market

- UAE Market

- Rest of world (remaining countries of the LAMEA region) Market

-

Major Players Operating the Armored Vehicles

-

-

Rheinmetall AG

-

BAE Systems

-

General Dynamics

-

Oshkosh Corporation

-

Hanwha Group

-

KNDS

-

Otokar Otomotive Ve Savunma Sanayi

-

Textron Inc.

-

Krauss-Maffei Wegmann

-

Denel SOC Ltd.

-

Textron Systems Corporation

-

Elbit Systems

-

Patria Group

-

FNSS Savunma Sistemleri AS

-

Arquus

-

Hyundai Rotem

-

Frequently Asked Question About This Report

Armored Vehicles Market [UP685A-00-0620]

Armored Vehicles Market size was estimated at USD 40.5 billion in 2025.

Armored vehicles market growth is driven by increasing global defense spending, ongoing military modernization programs, rising geopolitical tensions, and advancements in AI, autonomous, and hybrid vehicle technologies.

Armored vehicles market has the potential for growth and the market is projected to reach USD 53.7 billion by 2033, growing at a CAGR of 3.6% from 2026 to 2033.

Major players are Rheinmetall AG, BAE Systems, General Dynamics, Oshkosh Corporation, Hanwha Group, KNDS, Otokar Otomotive Ve Savunma Sanayi, Textron Inc., Krauss-Maffei Wegmann, Denel SOC Ltd., Textron Systems Corporation, Elbit Systems, Patria Group, FNSS Savunma Sistemleri AS, Arquus, Hyundai Rotem among others.

Europe has become the leading global market for armoured vehicles, primarily driven by the Russia–Ukraine conflict coupled with push from the US government to European Nato countries to increase their defence budget initially to 2% but eventually to 5% of the GDP by 2035

Infantry Fighting Vehicles (IFVs) led the market, accounting for approximately 31% share in 2025.

Wheeled armored vehicles dominated global revenues, capturing around 73.5% share in 2025.

Conventional propulsion systems remained dominant, contributing over 85% of total market revenue in 2025.

The OEM segment held the largest share of the market in 2025.

Related Reports

Why GMI Research